Shares Magazine - Fundsmith success: Smithson doubles in value in three years

The trust has been a strong performer and is sticking to a tried and tested strategy

Investors who backed Fundsmith’s investment trust Smithson (SSON) at launch October 2018 have now doubled their money.

Their faith in the Fundsmith investment process has been vindicated, and proof they were right to put their money with Smithson despite it being run by a fund manager (Simon Barnard) who, at the time of launch, was unknown to the retail market.

Terry Smith defined the Fundsmith investment process in 2010 with the launch of the Fundsmith Equity Fund (B41YBW7), which has since gone on to deliver superior returns. The ‘buy good companies, don’t overpay, do nothing’ strategy worked for large caps, so Smith thought it could be replicated in the mid and small-cap space, being the premise of Smithson.

Having debuted at £10 three years ago, Smithson hit the £20 share price level on 10 November 2021. Impressively this performance has been delivered against the backdrop of the pandemic and a year just gone which has seen a rotation out of the quality names which Smithson targets and into value. It also proved that Terry Smith didn’t need to be behind the driving wheel to make the trust a success.

Talking to Shares, manager Simon Barnard says: ‘We’re long-term investors with at least a 10-year time horizon. Even if there’s market rotation over two or three years – it might feel like a long time at the time, but it wouldn’t change our approach.

‘Ironically even this year when many commentators have been talking about a shift towards value we are only slightly behind the benchmark and haven’t fared badly in this environment.’

LAYING THE FOUNDATIONS

The foundations for Smithson’s success were laid early on. Before the trust was launched the team behind it spent a year analysing the universe of stocks – getting rid of the sectors which they didn’t like, including airlines, automotive firms, commodities-related businesses, real estate and regulated industries such as utilities.

That left 150 names which it went through with a fine-tooth comb, looking for high and sustainable returns on invested capital and margins, good free cash flow generation and strong free cash flow growth as well as evidence these metrics could be maintained over the next decade.

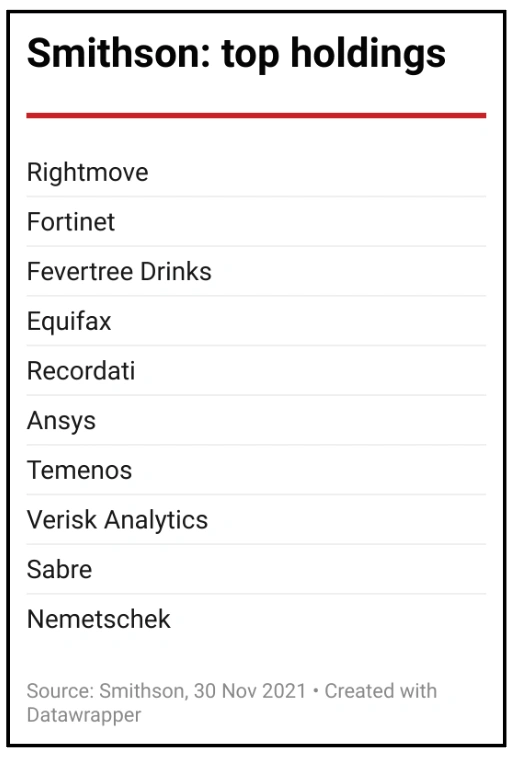

This distillation process resulted in a concentrated portfolio. At present there are 31 holdings, and the emphasis is on capital gains rather than dividends.

It invests in smaller-sized companies rather than outright small caps. The median market cap of Smithson’s holdings is a still chunky £9.9 billion. The ongoing charge is 1%.

Barnard says the increased scale of the trust, now valued by the market at £3.3 billion, isn’t creating any problems just yet.

If Smithson wanted to put 3% of its portfolio into a £2 billion company, it would need to buy a £99 million stake. That is nearly 5% of the company, which is a meaningful purchase, and equally this could be a challenge to offload in one go.

‘We have been able to buy new positions and sell out of others which would be the main mark of any issues arising,’ insists Barnard.

‘Because of our closed-ended structure we’ll never be forced to sell anything. We’re a long way off from having a problem in terms of capacity,’ he adds.

PORTFOLIO TURNOVER

The ‘do nothing’ part of the strategy was initially fully reflected in the turnover in Smithson’s portfolio – as Barnard notes in 2019 it was 6% which ‘is very similar to Fundsmith Equity’.

In 2020 it was more like 20% as the trust reacted to a volatile market. ‘We were very active around the March/April bottom in the market,’ says Barnard.

‘There was a lot which looked good value while some medical device names had doubled, so we trimmed our holdings there and put it into other names.’

Longer term the expected turnover rate is in the mid-single digits. Barnard dismisses the idea this is necessarily more difficult with smaller businesses despite their greater volatility.

Barnard says this long-term perspective means it hasn’t pursued a policy of buying lockdown winners. However, there are a few investee companies which have benefited during the pandemic and which he also believes have significant long-term potential.

For example, this includes Danish firm Ambu which makes single-use endoscopes. Barnard says: ‘Pretty much all existing endoscopes are reusable and obviously in today’s world with increased focus on the risk of infections Ambu had very strong growth last year and is penetrating so many different types of procedures.’

The other name he highlights is Wingstop which sells chicken wings. It was well-positioned for lockdown having launched a delivery service three years ago.

Barnard likes the fact it is a franchise business and can grow without using lots of capital and it is very profitable for individual franchisees – incentivising them to take on new franchises and helping to facilitate growth for the overall business.

SELLING STRATEGY

The ‘Do nothing’ part of the Fundsmith/Smithson investment strategy obviously has its limits and Barnard highlights several reasons why the trust might sell a stock. These include something fundamental changing in the investment case or valuation, though so far Smithson has only trimmed positions on the latter grounds rather than exiting completely.

And as Barnard concedes, sometimes they just get things wrong. He cites auto dealer software provider CDK Global which was in the portfolio at the trust’s launch. ‘We sold early on as when we got to know it better, we realised it wasn’t what we thought it was at the outset,’ Barnard says.

As the table shows, of its main rival trusts only one has outperformed Smithson since its inception - Herald (HRI) - while its ongoing charges figure sits somewhere in the middle. Smithson is also one of two trusts currently trading at a premium. This no doubt reflects the pull of Fundsmith’s lofty reputation.

In comparison, Herald has benefited from its focus on technology companies and is a significantly more diversified portfolio than Smithson, with 355 holdings.

Overall, Smithson has got off to a good start in its first three years, with decent market outperformance. Since inception the share price has risen by 93.6% to 30 November 2021, versus 45.7% from the MSCI World SMID index.

Shares views Smithson as an ideal component of a diversified portfolio, providing exposure to mid-cap stocks via a successful and proven investment strategy. You’re paying for active management and so far, the fund manager has deserved their fees as they’ve added significant value.